If you run finance at a community or regional bank, you may already know risk management statistics are more than headlines. They’re the inputs that shape pricing, liquidity buffers, capital choices, board reporting, and more.

Rates and depositor behavior can shift quickly; your planning cadence and the assumptions behind it must keep pace.

In this article, we bring together recent statistics, research, and many industry insights to help you benchmark today’s environment and decide where to focus.

You’ll see how peers are expanding scenario sets (including dynamic paths), tightening liquidity practices, and rethinking integration between asset and liability management (ALM) and planning.

The goal is to achieve faster, shared insight across finance and risk, so asset-liability committee (ALCO) conversations shift from “what happened” to “what we’ll do next.”

Table of Contents

- Global Risk Management Market Statistics

- Balance Sheet Risk Management in Banking Statistics

- Risk Preparedness and Resilience Statistics

- Regulatory and Compliance Statistics

- Stress Testing and Capital Adequacy Statistics

- Technology and Data in Risk Management Statistics

- Turn Risk Insights into Strategic Advantage

- FAQ: Risk Management

Disclaimer: All findings and statistics attributed to Empyrean Solutions in this article come from our extensive research, as detailed in our 2025 Empyrean Trends in Financial Risk Management and our 2025 Bank Risk and Performance Management Survey.

Global Risk Management Market Statistics

Finance leaders are navigating faster rate shifts and more volatile depositor behavior due to the recent unpredictable economy. This results in more frequent risk and performance assessment.

- The global risk management software and services market was $15.4 billion in 2024 and is projected to grow to $51.97 billion by 2033, a 14.6% compound annual growth rate (2025-2033). (Grand View Research)

- The average cost of a data breach globally in 2024 was $4.88M and $6.08M in the financial services sector, 22% higher than the global average. (IBM)

- 32% already integrate ALM with budgeting tools and another 28% plan to, signaling rising adoption of integrated risk and finance platforms. (Empyrean Solutions)

- Among Empyrean respondents preparing for falling rates, 51% keep their current strategy, 27% adjust their balance-sheet strategy, and 20% run dynamic forecasts. (Empyrean Solutions)

- U.S. banks’ deposit costs are projected to average 2.03% in 2025, still elevated versus the prior five-year average (0.9%). (Deloitte)

Empyrean ALM and Budgeting & Planning bring enterprise-grade analysis to mid-market institutions (without piling on complexity), so finance leaders like you can evaluate scenarios quickly and act with confidence.

Balance Sheet Risk Management in Banking Statistics

With deposit behavior shifting faster than it used to, balance-sheet decisions can’t wait for year-end plans.

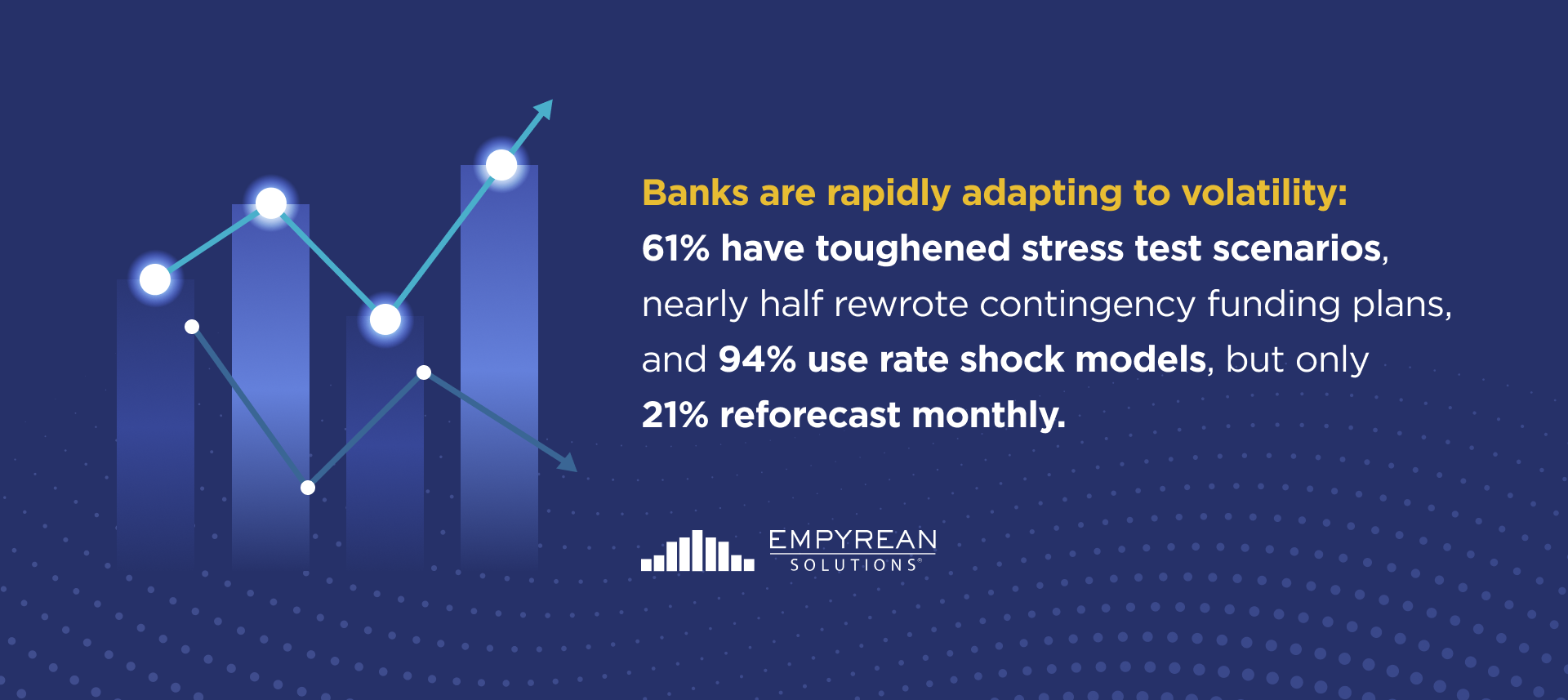

- Recent findings indicate that 59% of institutions are adjusting their balance-sheet strategy, and 67% are using dynamic scenario analysis; yet, only 21% reforecast monthly, which slows decision-making speed in volatile markets. (Empyrean Solutions)

- How banks build deposit assumptions for ALM (2025): 36% model internally, 31% use a third-party study, and 28% outsource to their ALM provider. (Empyrean Solutions)

- Refresh cadence for deposit assumptions (2025): 54% update annually, 33% quarterly, and 13% monthly, which is essential for keeping deposit betas current. (Empyrean Solutions)

- ALM scenario breadth (2025): 94% run parallel shocks, 75% include non-parallel shocks, and 50% add dynamic rate forecasts — wider paths to test net interest margin (NIM) and liquidity. (Empyrean Solutions)

- Funding mix watch-outs (FDIC, Q3 2024): Domestic deposits increased 1.1% quarter-over-quarter, with estimated uninsured deposits rising 2.7%, while brokered deposits declined 3.6%. These changes shape liquidity buffers and pricing. (FDIC)

- Behavioral-assumption stress testing (2025): Banks stress prepay/beta/decay quarterly (33%) or annually (54%); only 2% do this monthly, an area to tighten when funding is volatile. (Empyrean Solutions)

- Earnings pressure markers (FDIC, Q3 2024): Industry NIM increased seven basis points to 3.23% quarter over quarter, while the net charge-off ratio was 0.67%, still elevated versus prepandemic averages — key drivers for Profitability analysis. (FDIC)

Empyrean’s Deposit Analytics (for funding mix and betas) and Profitability (to see margin and return impacts) help finance teams recalibrate more often and brief ALCO with one version of the numbers. For process guidance, see Empyrean’s best practices on balance sheet risk and compliance.

Risk Preparedness and Resilience Statistics

When risk moves fast, boards and ALCOs need the same facts at the same time.

- Risk budgets are tight: 73% report funding constraints for emerging-risk identification, 75% for advanced monitoring, and 71% for third-party services, according to PwC’s Pulse Survey. (PwC)

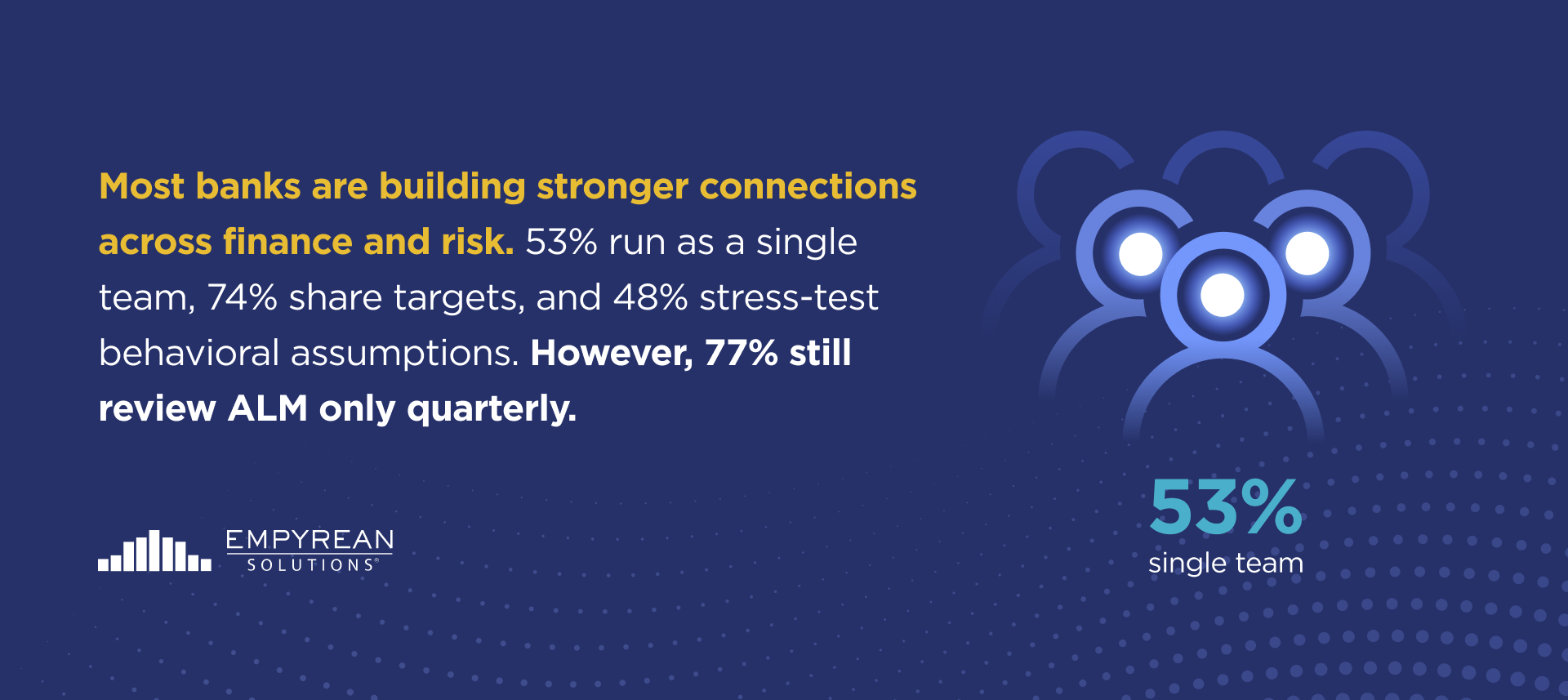

- 53% of institutions operate as a single team across finance, treasury, and accounting, while 18% maintain separate functions — a structural choice that impacts the speed and consistency of board reporting (2025). (Empyrean Solutions)

- Assumption sharing is gaining traction: 74% share balance-sheet targets, 62% share rate assumptions, and 53% share prepayment assumptions between ALM and planning. (Empyrean Solutions)

- 71% of audit committees now discuss cybersecurity quarterly, signaling a more routine approach to risk reviews at the board level. (Deloitte)

- Nearly half (48%) proactively test behavioral assumptions, and 41% say those results shape strategic decisions, linking model outputs to executive actions. (Empyrean Solutions)

- ALM simulations are still primarily conducted quarterly (77%), with 31% running monthly and 5% on an intra-monthly basis, setting the cadence for internal stress reviews and board updates. (Empyrean Solutions)

Empyrean helps finance and risk leaders work from a single source of truth, connecting ALM, Liquidity Stress Testing (LST), Planning, and Profitability, so decisions are quicker and easier to defend at the board level.

Regulatory and Compliance Statistics

Regulatory pressure is rising, but your board cares most about clear, consistent decision support.

- Empyrean’s 2025 survey reveals a shift from “check-the-box” compliance, with only 25% naming regulatory compliance as their primary objective. The modeling focus centers on liquidity (80%), earnings impact (77%), and interest rate risk (75%). (Empyrean Solutions)

- Basel III “endgame” would lift CET1 requirements 16% and RWAs 20% for large bank holding companies (phased 2025-2028). (Deloitte)

- The FDIC’s Problem Bank List rose to 68 institutions in Q3 2024 — about 1.5% of all banks — which is a reminder that supervisory risk remains elevated. (FDIC)

- OCC adjusted maximum civil money penalties in 2024 (inflation update), reinforcing the cost of control gaps. (Federal Register)

- Media roll-ups of Finbold’s data indicate $4.5B in global bank fines in 2024, with the U.S. accounting for 90%; most cases are tied to AML, bank secrecy, and consumer-protection violations. (Investment Executive)

Empyrean’s integrated framework helps finance and risk teams reduce reconciliations across siloed reports, enabling leaders to act with confidence. For a deeper look at practical policy-to-performance alignment, refer to our guide on asset and liability management.

Stress Testing and Capital Adequacy Statistics

Community and regional banks are using stress testing as a planning tool, not just a compliance exercise.

- Federal Reserve stress tests show that large banks would remain above minimum capital requirements under a severe recession — providing valuable context when benchmarking capital resilience. (Federal Reserve Board)

- 77% of surveyed institutions run ALM simulations quarterly, 31% monthly, and 5% intra-month. (Empyrean Solutions)

- Scenario breadth is widening: 75% run nonparallel shocks; 50% include dynamic forecasts; 8% add stochastic simulations. (Empyrean Solutions)

- Since 2023, 61% of LST scenarios have increased severity, 46% have revised contingency funding plans to reflect faster deposit runoff, and 36% have adjusted the deposit strategy. (Empyrean Solutions)

- Behavioral-assumption stressing remains infrequent for many institutions: 33% do it quarterly, 54% annually, and only 2% monthly. (Empyrean Solutions)

Empyrean’s ALM and liquidity stress testing modules enable you to model forward-looking scenarios tailored to your balance sheet and depositor behavior, while deposit analytics help you pressure-test funding assumptions before they yield results.

Technology and Data in Risk Management Statistics

Modern risk teams require faster modeling and more accurate reporting.

- Deloitte predicts that AI tools are set to revolutionize software engineering in the banking industry, potentially reducing software investment costs by 20% to 40% by 2028. (Deloitte)

- Many banks and credit unions are making strides to align their teams and processes:

- 72% report resource alignment across finance and treasury areas, and 74% share assumptions or results between their ALM and planning processes. (Empyrean Solutions)

- Yet, only 33% indicate that their tools across these areas are actually integrated. (Empyrean Solutions)

- How institutions calculate “above-margin” items in planning: 51% use instrument-level cashflows; 28% feed results from ALM; 11% general ledger (GL) + runoff assumptions; 9% GL averages. (Empyrean Solutions)

- Assumption sharing between ALM and planning: 74% share balance-sheet targets; 62% rate assumptions; 53% prepayments. (Empyrean Solutions)

- Manager input methods: 79% collect via meetings, email, phone; 56% via Excel templates; only 18% directly in a budgeting tool — a sign of manual friction. (Empyrean Solutions)

Empyrean is a cloud-native platform built for banks and credit unions. Its integrated framework helps teams run scenarios quickly and reuse the same data, rules, and results across ALM, planning, and profitability analytics.

Turn Risk Insights Into Strategic Advantage

The risk management statistics in this guide point to a clear pattern: Investment in enterprise risk management is rising, cyber and liquidity remain top concerns, leadership is more involved in risk choices, and banks are adopting modern tech to move faster.

Staying ahead means utilizing integrated, data-driven platforms that connect ALM, liquidity, planning, and profitability, enabling your team to act with confidence.

Discover how Empyrean ALM facilitates scenario analysis across rates, deposits, and balance sheet strategy. Explore the broader platform at Empyrean Risk Management.

Are you ready to take the next step?

See how Empyrean can centralize your risk, finance, and performance data for faster, more confident decisions

FAQ: Risk Management

What Is Risk Management in Banking?

Risk management in banking is the process of spotting, measuring, monitoring, and controlling risks that can affect earnings and capital. It covers how deposits behave, where funding comes from, how rates move, and how credit quality shifts.

Strong programs link models to decisions: pricing, liquidity buffers, capital plans, and growth choices.

What Are the Main Types of Financial Risk?

Banks manage several categories at once:

- Credit risk covers borrower repayment and concentrations.

- Interest-rate risk covers margin and value changes when rates move.

- Liquidity risk refers to the ability to meet cash needs under stress.

- Market risk encompasses movements in securities prices and spreads.

- Operational risk covers process, people, third parties, and cyber.

Many teams also track strategic and reputational risk because they influence board decisions and regulator expectations.

How Often Should Banks Update Their Risk Models?

At a minimum, refresh assumptions and scenarios quarterly, with monthly updates when funding, rates, or credit metrics move. Reforecast when stress indicators change, including deposit runoff, betas, prepayments, charge-offs, and local economic data.

Keep ALM, liquidity stress testing, and planning on the same cadence, so finance and risk use one forecast in ALCO and board reports. This rhythm shortens decision time and reduces surprises in earnings.

What Tools Can Help With Bank Risk Management?

Use an integrated tool set that shares data and assumptions. Empyrean is one such platform, combining multiple risk management capabilities:

- ALM runs interest-rate and balance-sheet scenarios.

- Liquidity Stress Testing evaluates cash sources, runoff, and contingency actions.

- Deposit Analytics tracks mix, betas, and behavior.

- Budgeting & Planning turns model outputs into forecasts and reforecasts.

- Profitability shows how risk outcomes affect margin and returns.

Empyrean brings these together, so chief finance officers (CFOs) can brief leadership with one version of the numbers.